All Categories

Featured

Table of Contents

Degree term life insurance policy is among the most affordable coverage choices on the market since it offers standard defense in the kind of survivor benefit and just lasts for a collection amount of time. At the end of the term, it ends. Entire life insurance policy, on the various other hand, is considerably much more pricey than degree term life because it does not run out and comes with a money worth attribute.

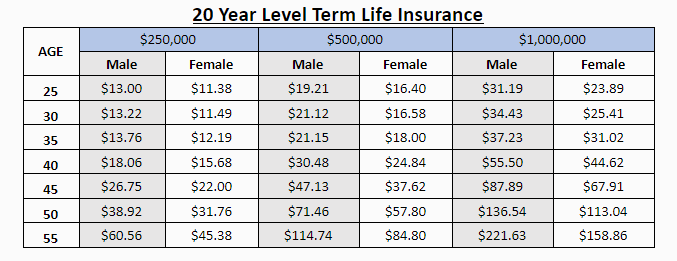

Prices may vary by insurance firm, term, insurance coverage amount, health and wellness class, and state. Not all policies are readily available in all states. Rate illustration legitimate since 10/01/2024. Level term is a terrific life insurance policy option for the majority of individuals, however depending upon your protection demands and individual circumstance, it could not be the most effective fit for you.

Level Term Life Insurance Companies

Annual renewable term life insurance policy has a regard to just one year and can be renewed each year. Yearly renewable term life premiums are initially lower than degree term life premiums, yet prices go up each time you restore. This can be a good alternative if you, for instance, have just stop smoking and require to wait 2 or three years to make an application for a level term plan and be qualified for a reduced rate.

With a reducing term life plan, your death advantage payout will certainly reduce gradually, yet your payments will certainly stay the exact same. Decreasing term life policies like home mortgage security insurance coverage typically pay to your loan provider, so if you're trying to find a plan that will certainly pay to your enjoyed ones, this is not a great fit for you.

Raising term life insurance policy policies can aid you hedge versus rising cost of living or plan financially for future children. On the other hand, you'll pay even more upfront for less coverage with a boosting term life plan than with a level term life policy. If you're uncertain which type of plan is best for you, collaborating with an independent broker can aid.

What are the benefits of 30-year Level Term Life Insurance?

Once you've decided that level term is best for you, the next action is to acquire your plan. Right here's how to do it. Calculate exactly how much life insurance you need Your coverage quantity must offer your household's long-lasting economic requirements, consisting of the loss of your earnings in the event of your fatality, along with financial debts and everyday expenses.

:max_bytes(150000):strip_icc()/dotdash-ask-answers-205-Final-7a1ca51b85d44e0d81dc7b46f919180d.jpg)

As you search for means to safeguard your economic future, you've most likely found a wide range of life insurance policy alternatives. Selecting the appropriate protection is a huge decision. You wish to find something that will certainly aid support your loved ones or the causes vital to you if something takes place to you.

Many people lean towards term life insurance policy for its simplicity and cost-effectiveness. Term insurance policy contracts are for a relatively brief, defined time period yet have choices you can customize to your requirements. Particular advantage choices can make your costs alter over time. Level term insurance coverage, nevertheless, is a kind of term life insurance policy that has regular payments and an imperishable.

How can Tax Benefits Of Level Term Life Insurance protect my family?

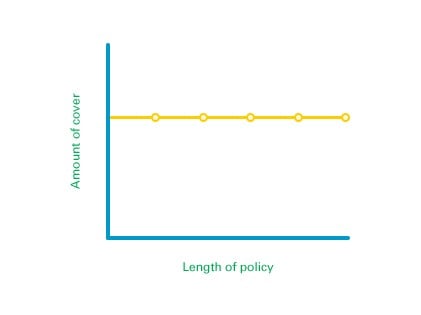

Level term life insurance policy is a subset of It's called "level" because your premiums and the benefit to be paid to your enjoyed ones stay the very same throughout the contract. You will not see any kind of modifications in price or be left questioning about its value. Some contracts, such as each year eco-friendly term, may be structured with premiums that increase in time as the insured ages.

They're figured out at the beginning and stay the very same. Having regular settlements can assist you better strategy and budget due to the fact that they'll never ever change. No medical exam level term life insurance. Dealt with death advantage. This is also evaluated the start, so you can understand exactly what survivor benefit amount your can expect when you die, as long as you're covered and up-to-date on premiums.

What is the best Tax Benefits Of Level Term Life Insurance option?

You agree to a fixed premium and death advantage for the period of the term. If you pass away while covered, your fatality benefit will certainly be paid out to liked ones (as long as your premiums are up to date).

You may have the choice to for an additional term or, extra likely, restore it year to year. If your agreement has an ensured renewability stipulation, you might not need to have a brand-new clinical examination to keep your insurance coverage going. Your costs are most likely to increase since they'll be based on your age at renewal time.

With this choice, you can that will certainly last the remainder of your life. In this case, once more, you might not need to have any new medical examinations, however costs likely will increase due to your age and new insurance coverage. Various business provide different alternatives for conversion, be sure to comprehend your options prior to taking this step.

Consulting with an economic expert also may assist you determine the path that lines up ideal with your general method. The majority of term life insurance policy is level term throughout of the agreement duration, yet not all. Some term insurance policy might come with a premium that raises in time. With decreasing term life insurance policy, your survivor benefit goes down in time (this kind is usually taken out to specifically cover a long-lasting financial debt you're paying off).

What are the top Level Term Life Insurance Companies providers in my area?

And if you're established for sustainable term life, after that your premium likely will go up every year. If you're discovering term life insurance policy and want to make sure simple and foreseeable economic security for your household, degree term may be something to take into consideration. As with any kind of type of protection, it might have some constraints that do not fulfill your needs.

Normally, term life insurance is more budget friendly than irreversible coverage, so it's an economical method to secure economic security. At the end of your agreement's term, you have several choices to continue or move on from protection, commonly without needing a medical exam (Level term life insurance for young adults).

How does Level Term Life Insurance Vs Whole Life work?

Similar to other type of term life insurance policy, when the agreement ends, you'll likely pay higher costs for coverage since it will certainly recalculate at your existing age and wellness. Repaired protection. Degree term supplies predictability. If your monetary scenario modifications, you might not have the essential protection and might have to acquire added insurance policy.

That doesn't indicate it's a fit for everybody. As you're looking for life insurance, here are a few vital factors to think about: Budget plan. One of the advantages of degree term protection is you understand the price and the death advantage upfront, making it easier to without bothering with rises in time.

Normally, with life insurance policy, the much healthier and more youthful you are, the a lot more budget-friendly the protection. Your dependents and monetary duty play a duty in identifying your insurance coverage. If you have a young family members, for instance, degree term can aid offer economic assistance throughout important years without paying for insurance coverage longer than needed.

{kind=link}

Latest Posts

Funeral Cover For Old Age

Life Insurance To Cover Final Expenses

Over 50 Funeral Insurance